Blog

Blog

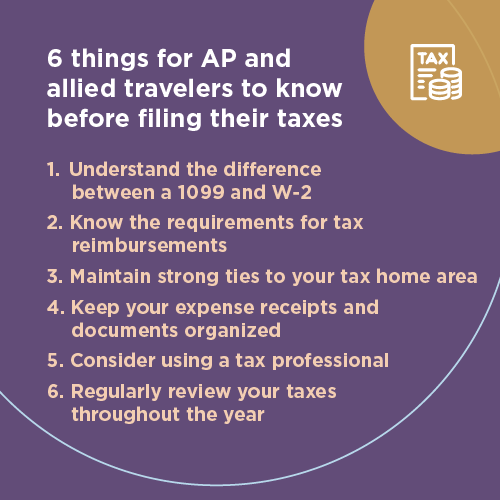

Working as an advanced practice (AP) locum or an allied traveler is a rewarding career, but the taxes that accompany working in multiple states can be a headache. That’s why ensuring you’re prepared and have done the planning is essential. Here are six things every traveler should know to make filing your taxes easier.

1. Understand the difference between 1099 and W-2

A 1099 employee is a self-employed independent contractor who is paid according to their contract and uses a 1099 form to report income on their tax return. At CompHealth, advanced practice providers and allied travelers are W-2 employees, which means we withhold income taxes for you and provide additional benefits like healthcare insurance and an employee assistance program. 1099 employees, on the other hand, typically must provide their own benefits.

Because income tax laws vary by state (and even some cities have an income tax), it’s always good to work with a professional tax advisor experienced with filing taxes in multiple states to make sure the appropriate withholding is happening. Even as a W-2 employee, you may need to set aside money yourself to pay taxes in some states, depending on their withholding requirements.

Make sure you’re covered: Find out which benefits CompHealth provides for AP locums and allied travelers

2. Know the requirements for tax reimbursements

For a traveler to qualify for travel reimbursements — for things such as airfare, mileage reimbursements, rental cars, temporary lodging, and meal per diems — they must meet three criteria:

- They must maintain a permanent tax home (see below for more information).

- They can’t commute from that tax home or work within commuting distance of the tax home.

- The assignment can’t last longer than one year.

If you don’t maintain a tax home or your travel assignment lasts more than one year, travel expenses can still be paid to you. However, the value of the expenses is considered taxable income, and all applicable payroll taxes will be withheld.

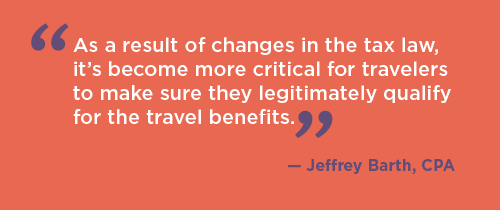

“As a result of changes in the tax law, it’s become more critical for travelers to make sure they legitimately qualify for the travel benefits,” shares Jeffrey Barth, a CPA with Tax Smart Advisors, a firm specializing in AP locums and allied travel taxes. “We had an individual who lived in Houston and commuted from one side of the city to the other. The IRS audited them and said it was a commutable distance since it was 52 miles from their home. The traveler received travel benefits but hadn’t claimed the income. The IRS not only required them to claim the income of their travel benefits and to pay taxes on it, they also had to pay pretty significant penalties.”

Barth also warns that because travel benefits can represent a significant portion of your total remuneration, benefits exceeding 25% of your income can be a fraud trigger for the IRS.

“The IRS can extend their audit for six years, and it raises the penalties they can apply,” Barth says. “They can apply a fraud penalty for substantial failure to underpay taxes. So, the penalties become larger, and the period which the IRS can go back and audit and review becomes extended.”

3. Maintain strong ties to your tax home area

Make sure you meet two of the three requirements needed for your tax home to qualify for untaxed travel reimbursements:

- Have regular employment in the area of your tax home.

- Spend at least 30 days at your tax home annually (it doesn’t have to be consecutive).

- Be financially responsible for the upkeep of your tax home when you’re away.

A few additional tips to prove your tax home is your permanent residence include:

- Don’t change your address when you’re traveling.

- Keep your driver’s license, car registration and insurance, and voter card from the area of your tax home.

- Use your credit card while you’re at home.

Get the details: How does locum tenens pay work for NPs and PAs?

4. Keep your expense receipts and documents organized

In case of an IRS audit, it’s important to keep copies of certain documents from your travel assignments, including:

- Copies of all contracts

- Mileage log

- Receipts

Barth recommends using an app, like the QuickBooks mobile app (iOS or Android), to capture copies of your receipts.

“If you do get into an audit situation, the IRS will want to see the actual receipt,” he says. “They don’t want to just see the charge going through the credit card; they want to see the receipt as the documentation.”

He also recommends consolidating your income and expenses by using a single credit card and bank account to make it easier to find transactions. Using an online storage platform like OneDrive, Google Drive, or iCloud is also helpful and allows you to access information while traveling.

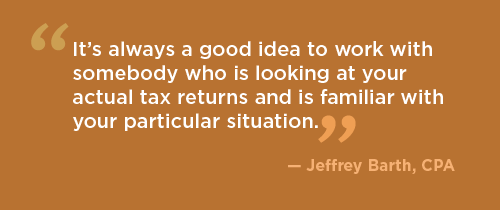

5. Consider using a tax professional

Working in multiple states makes filing your tax return more complicated, and not filing your taxes correctly can lead to paying penalties or may even negate your ability to maintain your permanent residence. To ensure your taxes are in order, use a tax professional who has worked with AP locums and allied travelers and has experience filing in different states.

“Every individual situation can be a little bit different, and so it’s always a good idea to work with somebody who is looking at your actual tax returns and is familiar with your particular situation,” Barth says.

6. Regularly review your taxes throughout the year (not just during tax season)

Failing to withhold enough federal and state taxes can subject you to significant penalties. To avoid this, Barth recommends doing a mid-year check-in with your tax professional sometime between July and November and asking:

- Am I withholding enough?

- What are the different states I’m working in withholding? Is it enough?

- Should I be paying quarterly or estimated federal or state taxes?

- Are there things I should be doing between now and the end of the year to mitigate taxes into the next year?

Following these tips will help remove the headache of filing your taxes. Still, nothing beats the peace of mind from working with a tax advisor experienced in filing taxes in multiple states to ensure everything is in order.

The information contained herein is general in nature and is subject to change. The tax information contained in this document is not intended to be used, and cannot be used, by any person as a basis for avoiding tax penalties that the IRS or any state may impose. We recommend each taxpayer seek advice from an independent tax advisor based on their circumstances.